On Retirement Income, Part 9: TIPS Q&A

TIPS investing is complicated! We answer some of your questions here.

TIPS investing is complicated! We answer some of your questions here.

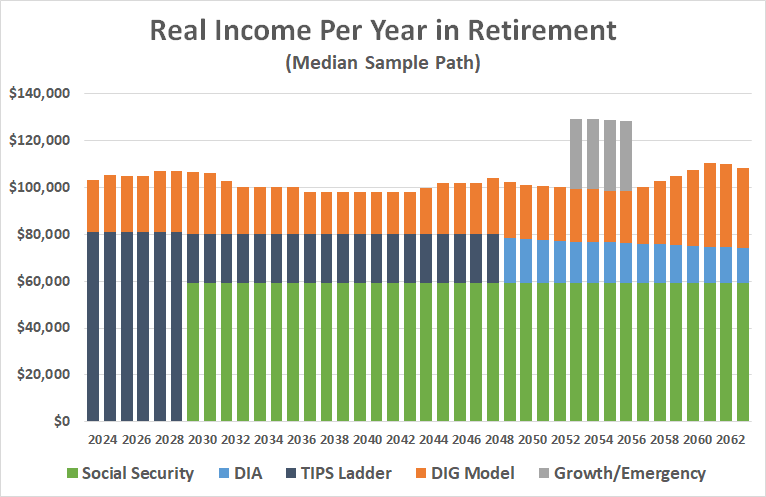

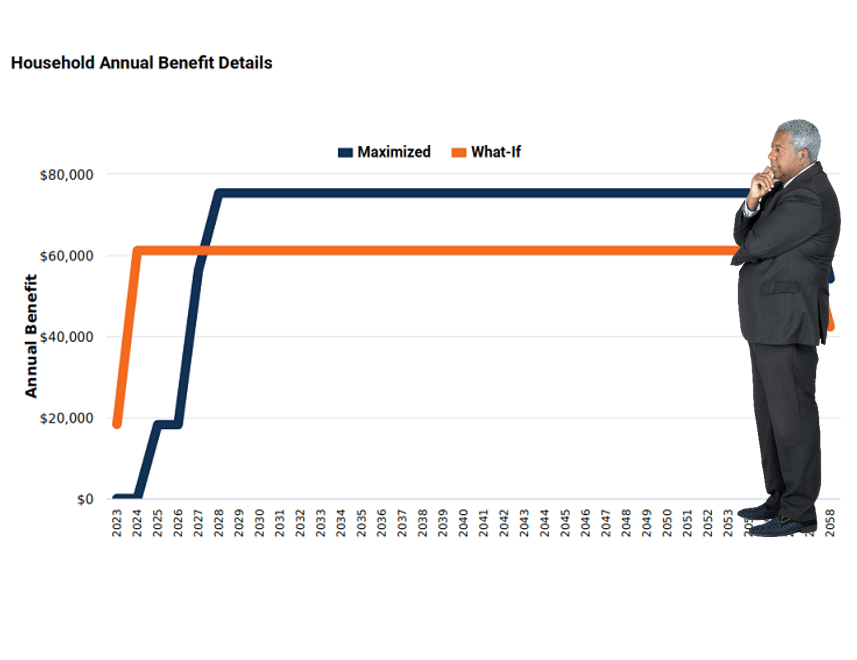

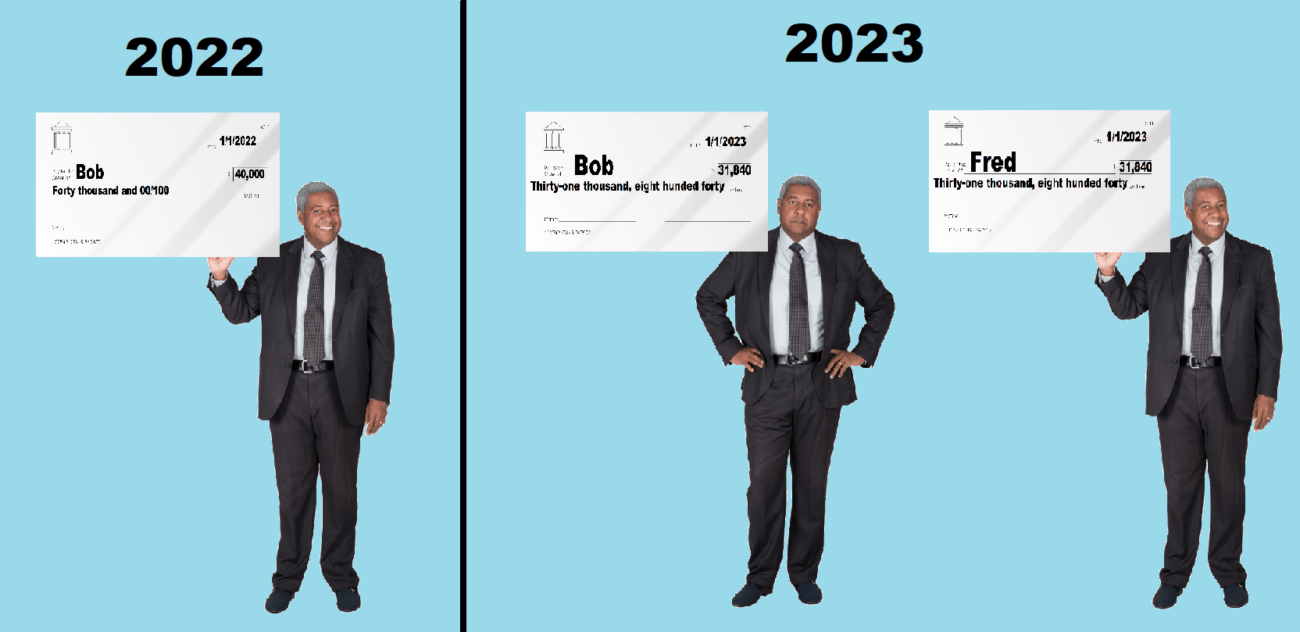

Well, it has been a while, but our fictional friends Bob and Fred are finally getting some attention again. We’re pulling their financial plan out of stasis to illustrate how we can (A) build an inflation-protected income bridge from retirement to age 70, enabling someone to maximize benefits by delaying Social Security claiming and (B) add a long-term stream of inflation-protected income on top of Social Security, to fill a gap between promised benefits and inflexible annual spending needs.

Lifetime inflation-protected income (up to age 100) from a mutual fund!

In Part 4, we get practical, demonstrating how discoveries from previous articles can be applied to a goals-based investment approach in retirement.

Guaranteed income from Social Security, pensions, and annuities can be the bedrock of a retirement income plan. But such guarantees are only useful if the guarantors can be trusted!

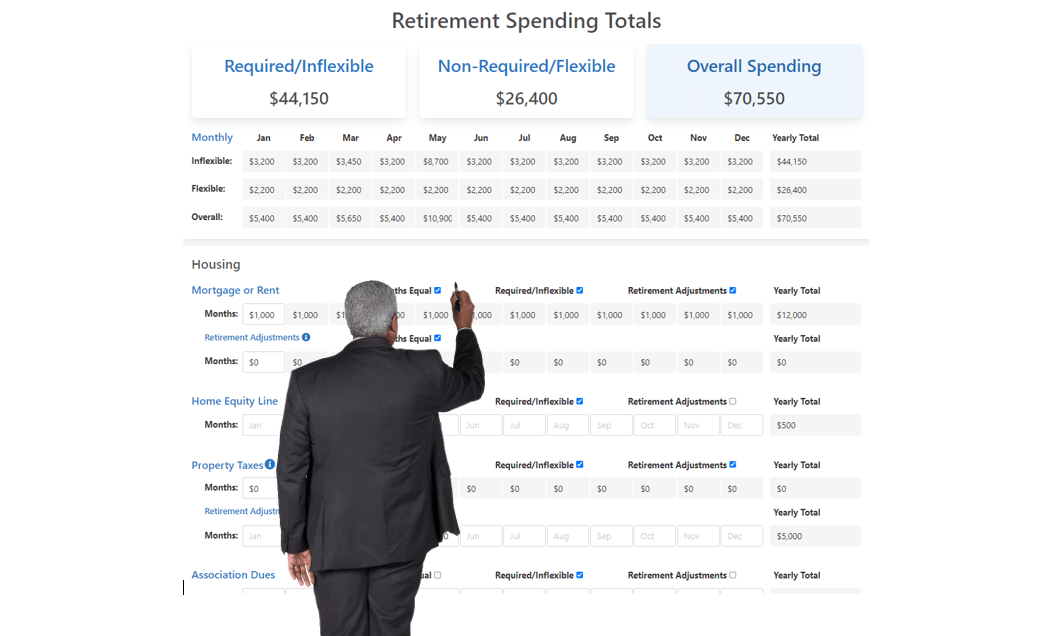

One of the most significant facets of “goals-based investing” is matching inflexible spending needs with secure income sources, most notably Social Security.

At Round Table, we practice “true goals-based investing.” Our process starts with understanding our clients’ goals, needs, fears, and broader financial picture.

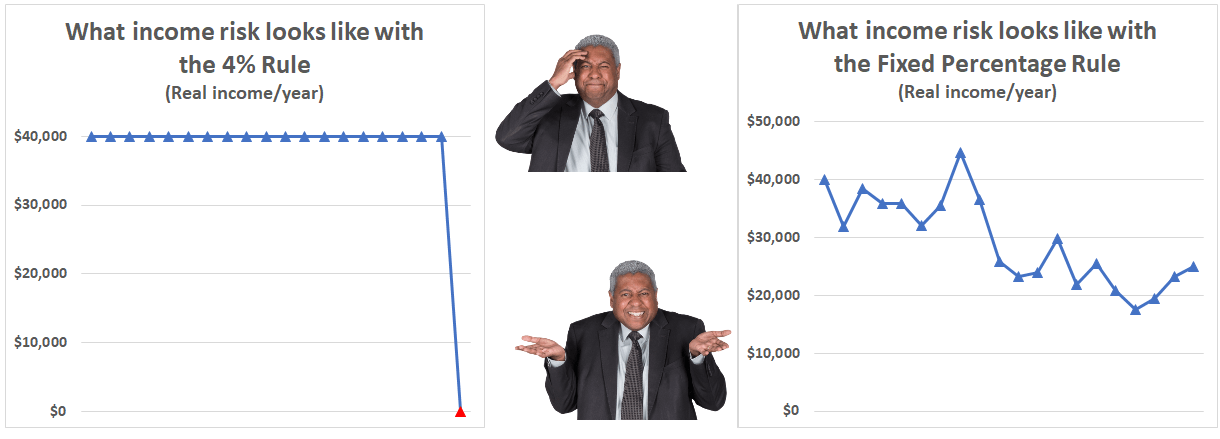

The “4% Rule” and “Fixed Percentage Rule” are opposites…but both involve risk, including a scary beast call “sequence-of-returns” risk.

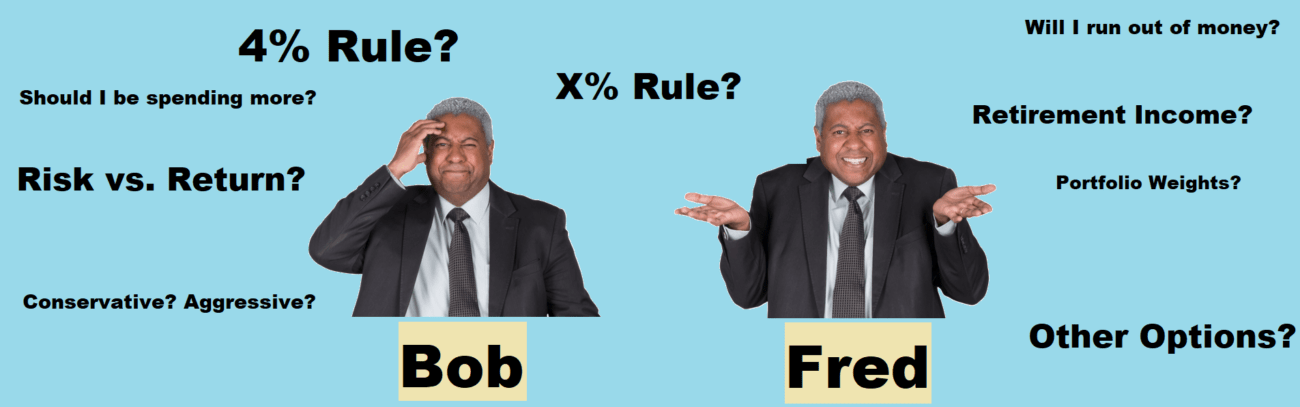

As “Bob and Fred’s Excellent Adventure” resumes, they hop in a time machine to try a completely opposite retirement income strategy. Does it wok better?

Let’s dig further into the facts and foibles of the 4% rule, as a launchpad for a broader discussion about retirement income.