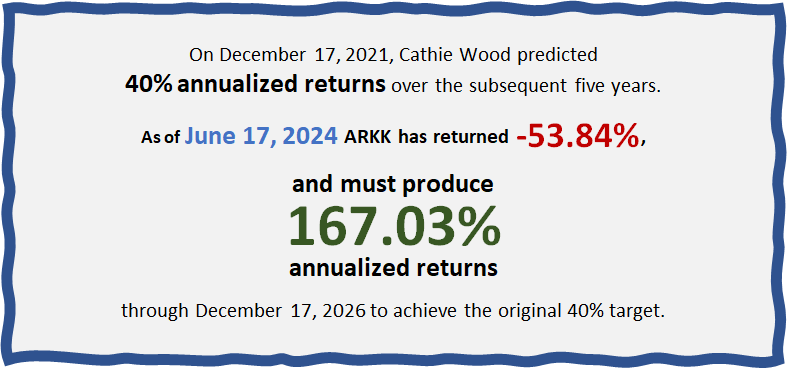

“There Is No Magic Investment Return Fairy!”

We’ve created a series of posts on LinkedIn exploring two fundamental postulates of stock market (or, more generally, risk asset) investing: The logic is simple:

We’ve created a series of posts on LinkedIn exploring two fundamental postulates of stock market (or, more generally, risk asset) investing: The logic is simple:

TIPS investing is complicated! We answer some of your questions here.

It’s tempting to say “the image says it all.” But there’s a whole Advisor Perspectives article because there are more insights to be gleaned from this example.

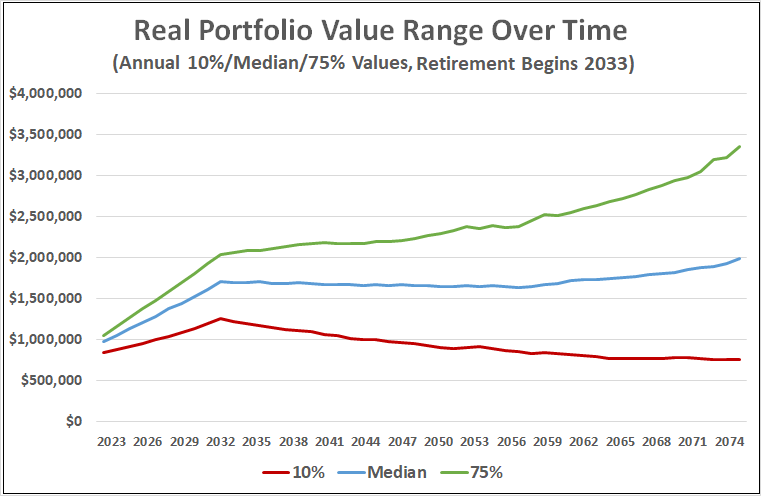

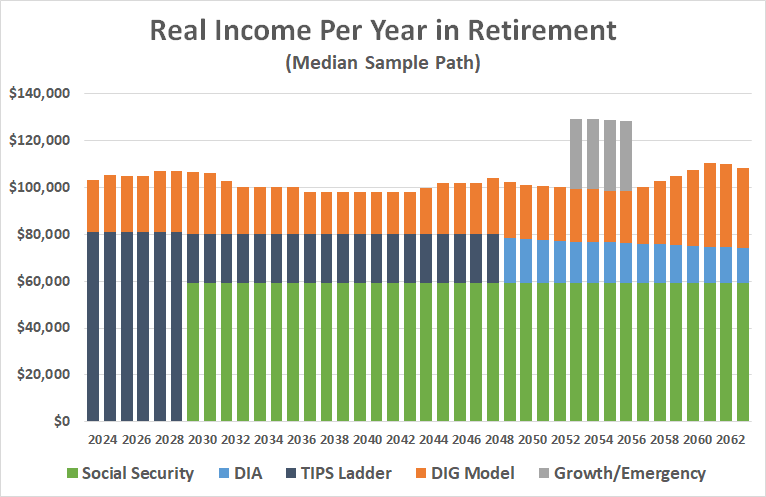

Well, it has been a while, but our fictional friends Bob and Fred are finally getting some attention again. We’re pulling their financial plan out of stasis to illustrate how we can (A) build an inflation-protected income bridge from retirement to age 70, enabling someone to maximize benefits by delaying Social Security claiming and (B) add a long-term stream of inflation-protected income on top of Social Security, to fill a gap between promised benefits and inflexible annual spending needs.

Lifetime inflation-protected income (up to age 100) from a mutual fund!

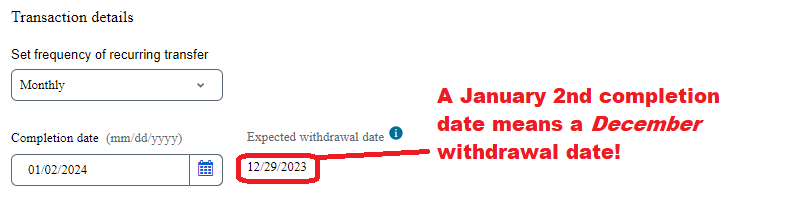

Advisors who set up recurring withdrawals at TD need to beware. With the transition to Schwab, those scheduled January withdrawals may take effect in December instead.

The final installment on Advisor Perspectives focuses on goals-based investing techniques pre-retirement.

In Part 4, we get practical, demonstrating how discoveries from previous articles can be applied to a goals-based investment approach in retirement.

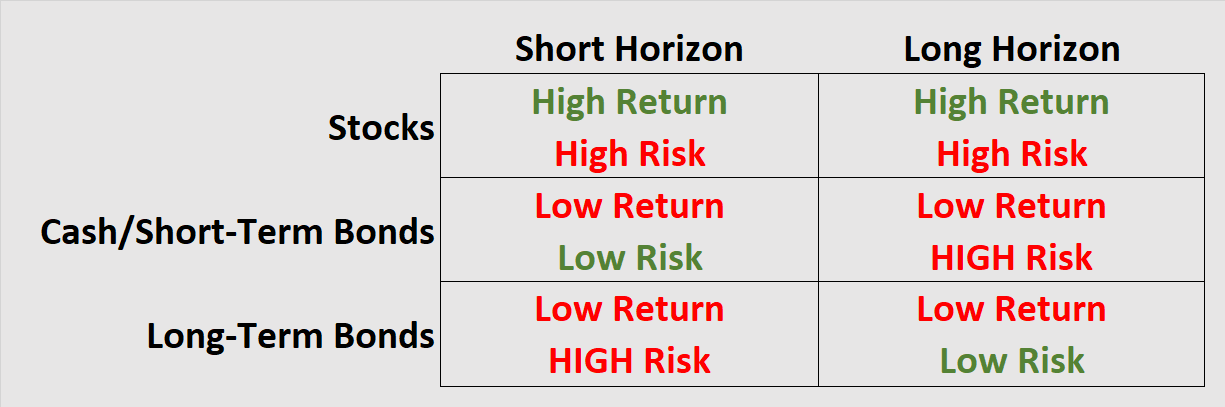

In investing, you can have safe present value OR safe future value, but not both!

Part 2 of “Long-Horizon Investing” on Advisor Perspectives takes a tour of the theoretical reasons why stocks must be risky at all horizons.