“There Is No Magic Investment Return Fairy!”

We’ve created a series of posts on LinkedIn exploring two fundamental postulates of stock market (or, more generally, risk asset) investing: The logic is simple:

We’ve created a series of posts on LinkedIn exploring two fundamental postulates of stock market (or, more generally, risk asset) investing: The logic is simple:

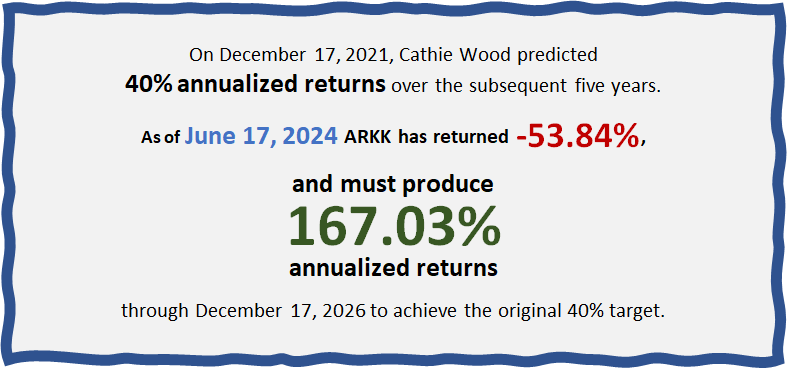

It’s tempting to say “the image says it all.” But there’s a whole Advisor Perspectives article because there are more insights to be gleaned from this example.

Guaranteed income from Social Security, pensions, and annuities can be the bedrock of a retirement income plan. But such guarantees are only useful if the guarantors can be trusted!

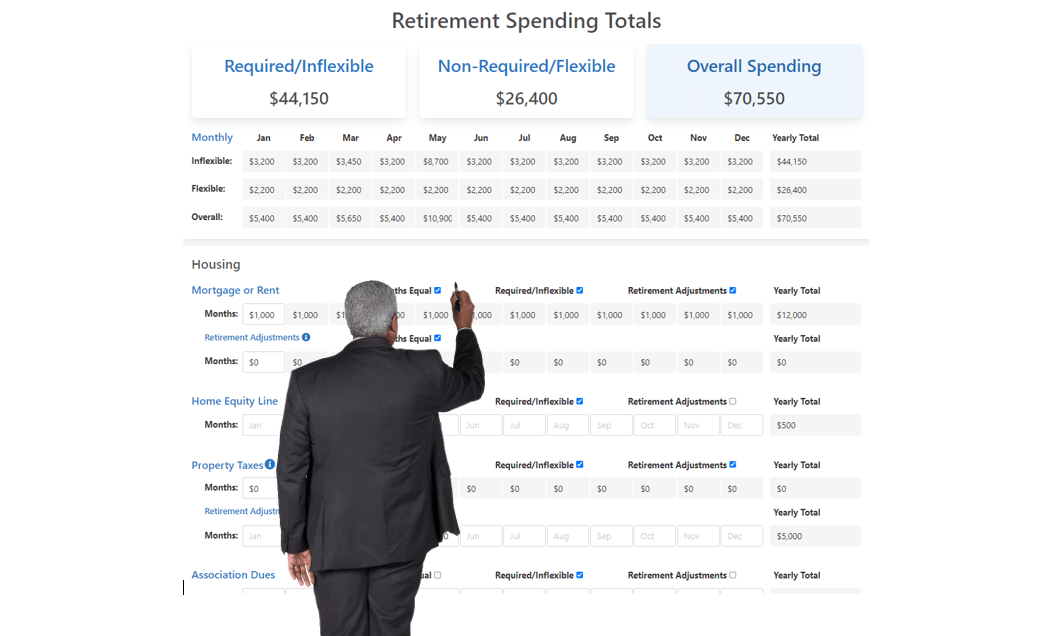

At Round Table, we practice “true goals-based investing.” Our process starts with understanding our clients’ goals, needs, fears, and broader financial picture.

As “Bob and Fred’s Excellent Adventure” resumes, they hop in a time machine to try a completely opposite retirement income strategy. Does it wok better?

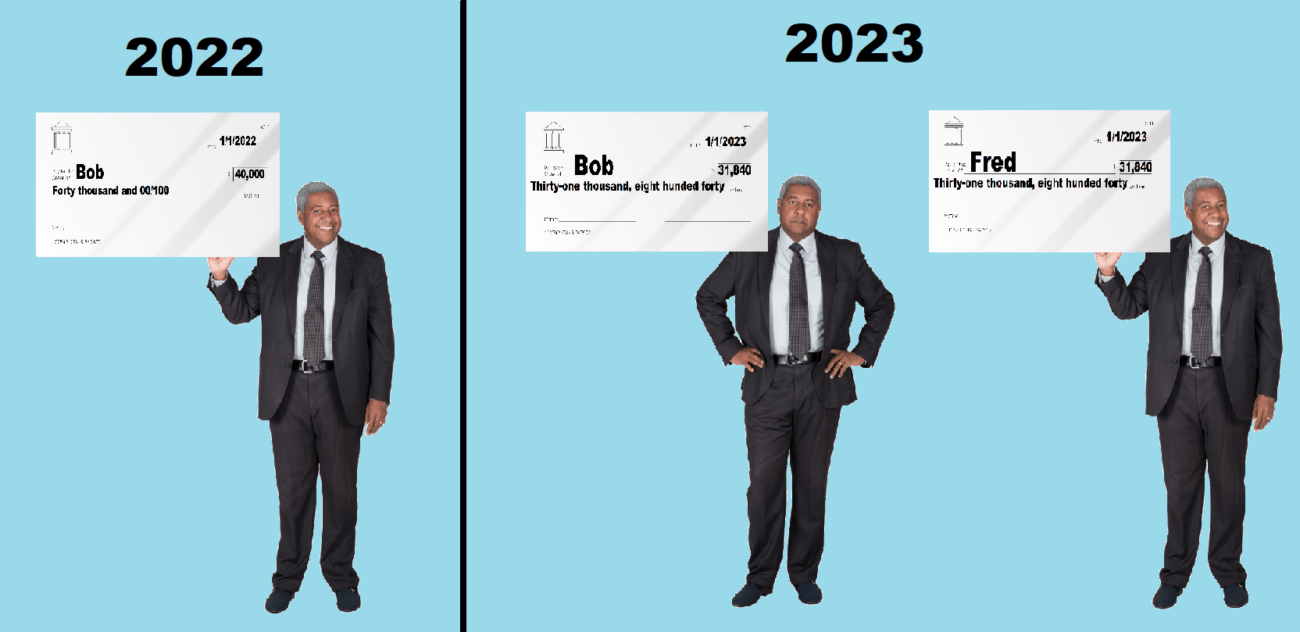

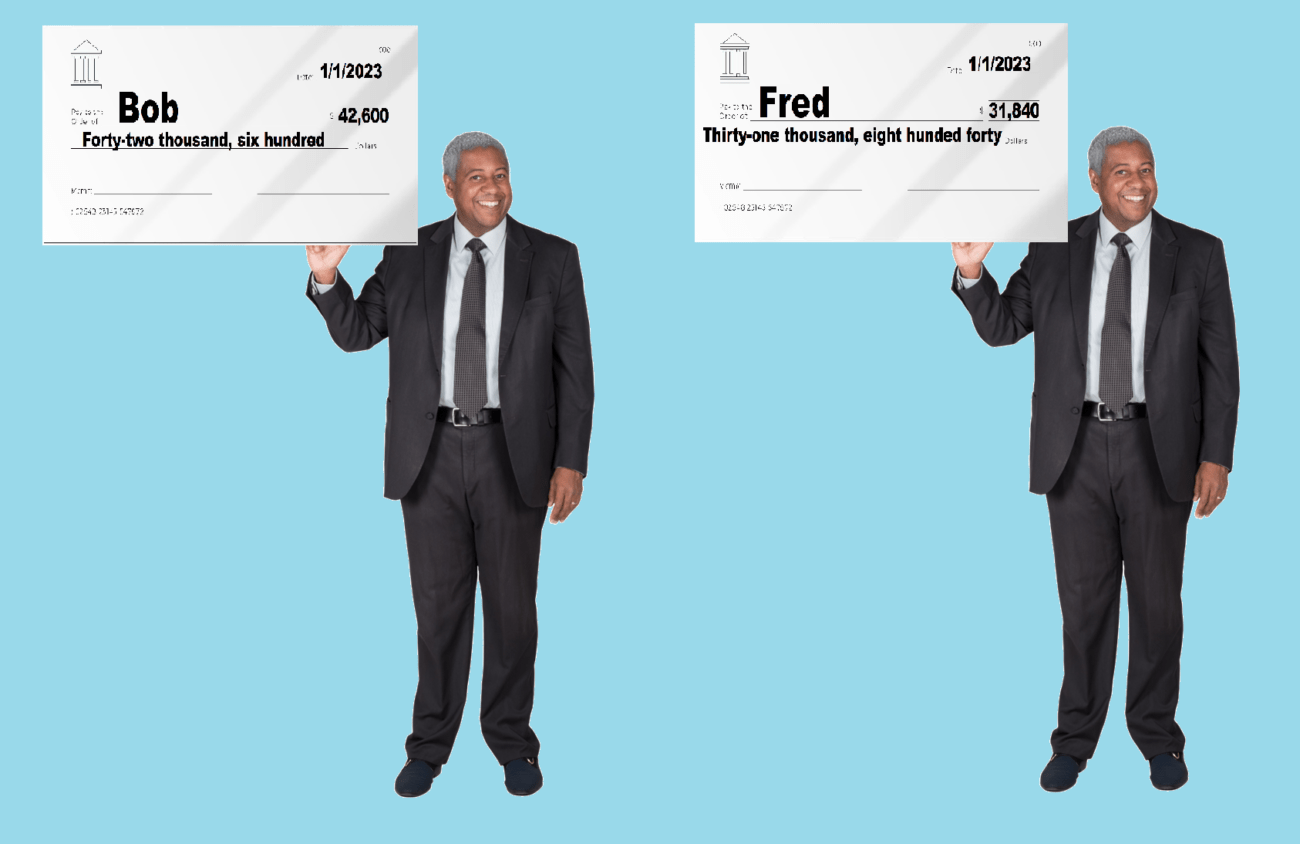

Twin brothers, same age, same assets, same everything…but one has a “safe withdrawal rate” 34% larger than the other?! Find out how that (could have) happened as Round Table’s latest article kicks off our series on retirement income.

October is the final month to take advantage of a 9.62% annualized rate for six months by purchasing “Series I Savings Bonds” (or “I-Bonds”) from the U.S. Treasury.

Measured with daily data, the S&P 500 Index (the usual stand-in for “the stock market” in the U.S.) is in its second bear market in just over two years. Measured with monthly data, the S&P 500 is still in a historic bull market that stretches back to 2009.

I-Bonds are government-guaranteed savings bonds that pay a fixed rate plus the recent inflation rate. From May through October 2022, these bonds pay 9.62% annualized, due to prevailing high inflation.