“Long-Horizon Investing, Part 4: Real-Life Applications in Retirement” on Advisor Perspectives

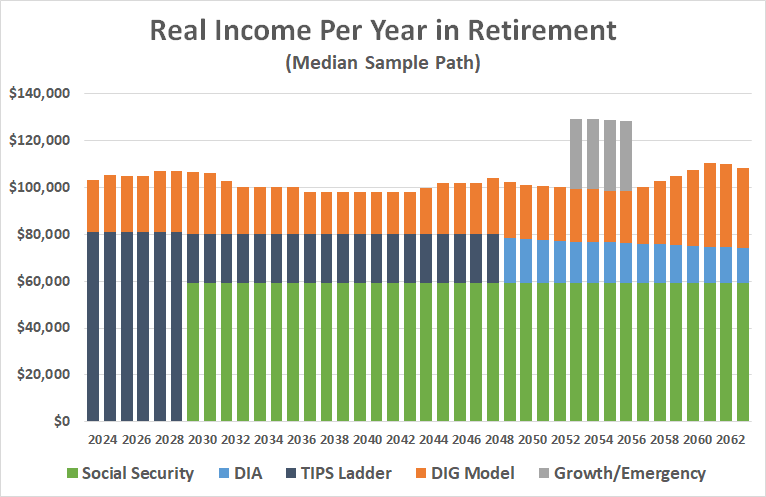

In Part 4, we get practical, demonstrating how discoveries from previous articles can be applied to a goals-based investment approach in retirement.

In Part 4, we get practical, demonstrating how discoveries from previous articles can be applied to a goals-based investment approach in retirement.

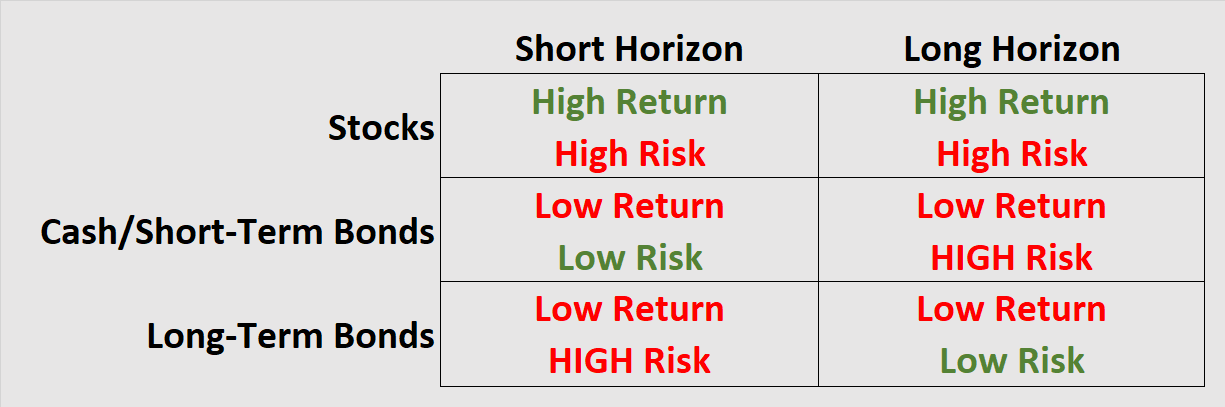

In investing, you can have safe present value OR safe future value, but not both!

I’m excited to announce the publication on Advisor Perspectives of the first article in a five-part series entitled “Long-Horizon Investing”!

The headline rate on I-Bonds has fallen below T-Bills, CDs, etc. Round Table presents a Kenny Rogers-inspired framework for considering your I-Bond options now.

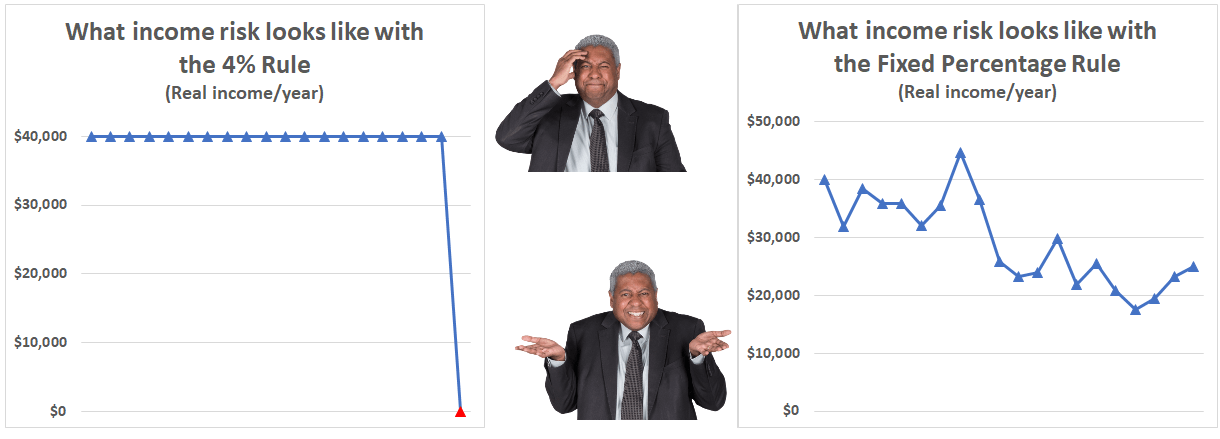

The “4% Rule” and “Fixed Percentage Rule” are opposites…but both involve risk, including a scary beast call “sequence-of-returns” risk.

As “Bob and Fred’s Excellent Adventure” resumes, they hop in a time machine to try a completely opposite retirement income strategy. Does it wok better?

Let’s dig further into the facts and foibles of the 4% rule, as a launchpad for a broader discussion about retirement income.

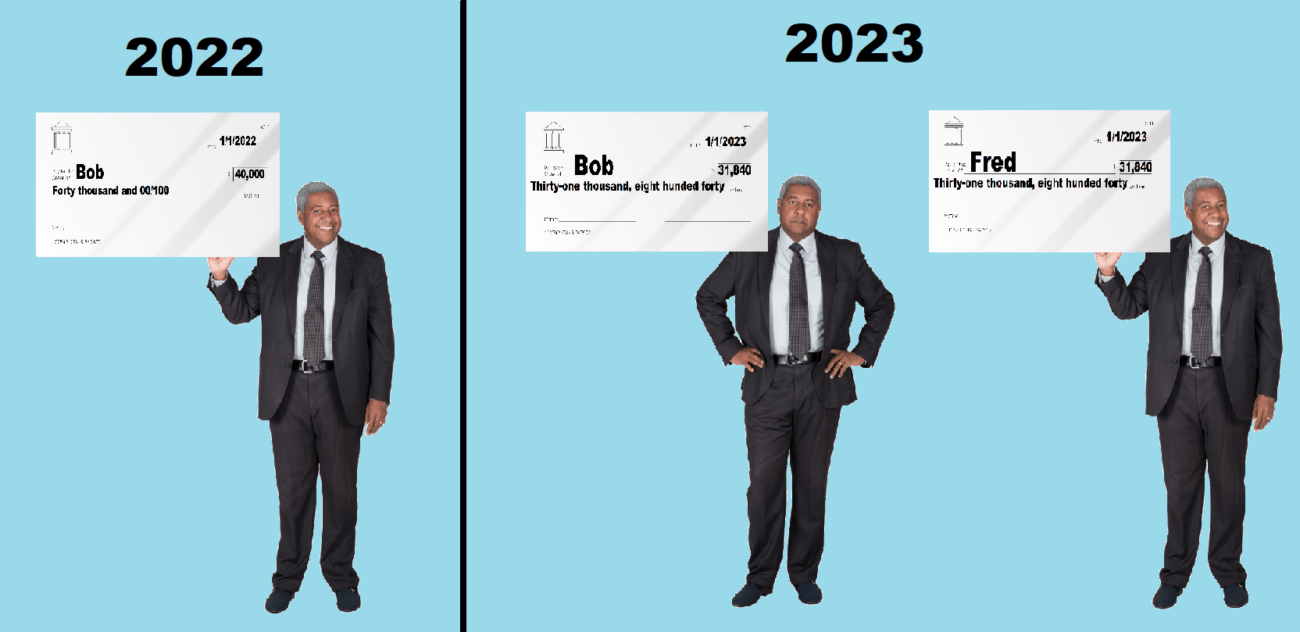

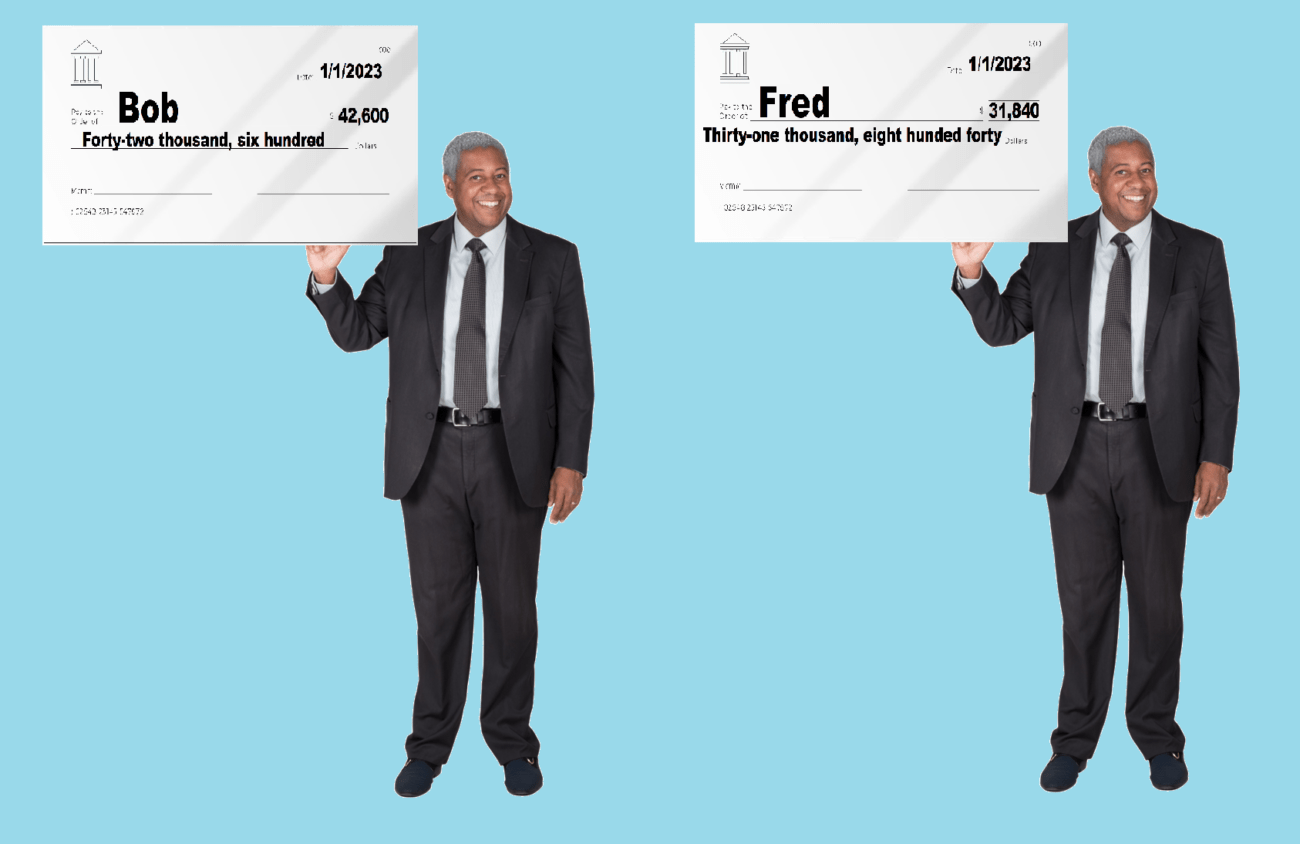

Twin brothers, same age, same assets, same everything…but one has a “safe withdrawal rate” 34% larger than the other?! Find out how that (could have) happened as Round Table’s latest article kicks off our series on retirement income.

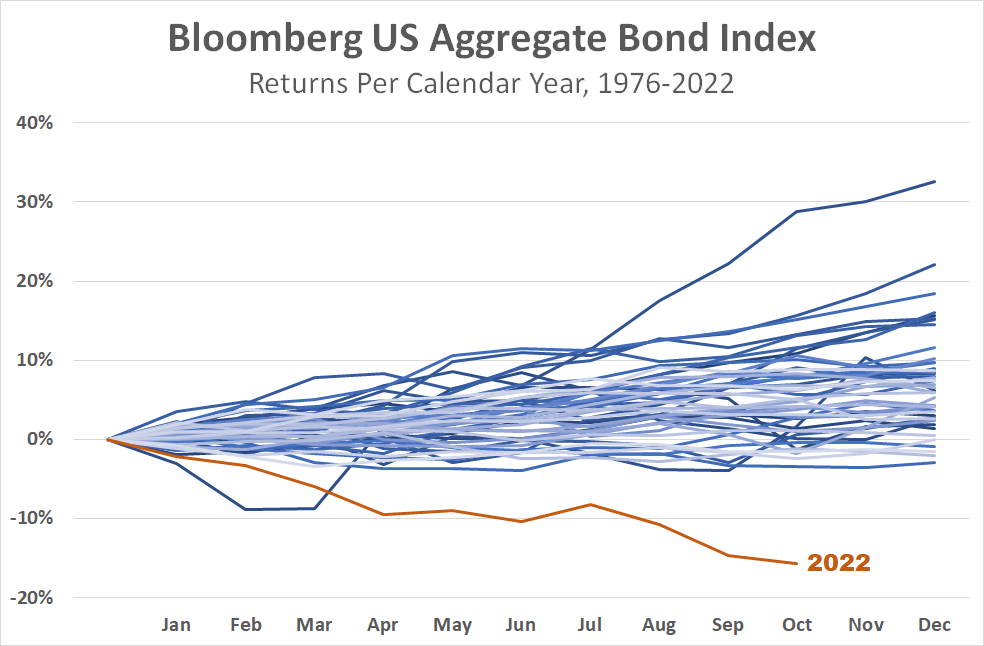

Bond markets are down a record amount in 2022. What happened, and is there any good news?

This article presents an in-depth compare/contrast between I-Bonds and TIPS, with basic facts and color commentary—including several surprising discoveries!